WITTCHEN S.A. (WTN.WA)

WITTCHEN S.A. (WTN.WA)

A founder-led and owned Polish producer of leather goods specialised in suitcases and travel accessories., selling for a P/E of 7, EV/EBIT of 5.6 and and a 30% discount to normalised intrinsic value.

Special thanks to Desi. You were the final push in making me go back to work and finish it.

Key Facts

Description: Wittchen is a Polish founder-owned and led leather goods and fashion business specialising in suitcases, travel accessories and apparel. It’s the domestic leader in Poland with a significant presence in Europe, especially in the central and eastern EU. They sell through both offline and online channels and use third-party marketplaces. Their products are much cheaper than almost all of the international more premium competition and they are also higher quality than local Polish cheap competitors. Wittchen was founded in 1990 in Poznań, Poland and is headquartered in Nowy Dwór Mazowiecki today (not that far from Warsaw).

Track record: Over the last 10 years Wittchen compounded revenue at an 18.7% CAGR (38.7% over the last 3 and 46.2% last year). It has also grown its BVPS at a 10-year 25.5% CAGR (14.5% over the last 3 years). Its ROIC improved from the 10-year average of 18.9% to a 3-year of 19.1% (last year was 32.2%). It has done all that while operating on a modest amount of debt, which it can easily pay off with 1-2 years of free cash flow.

Market cap: As of the 3rd of January 2024, its market cap is ~530 million PLN (~$133 million). It has declined slightly since January 1, 2024. It is also ~30% up from its 52-week low.

Valuation: WTN.WA trades at a TTM P/E of 7x (5-year average of 8.5x), EV/EBIT of 6.58x (5-year average of 8.81x) and at a ~30% discount to a conservatively calculated intrinsic value.

Business Overview

Background

Wittchen designs and sells various leather clothing accessories, clothes, shoes, and most importantly, luggage accessories like suitcases. The product range includes bags, wallets, travel accessories (suitcases, travel bags, cosmetic bags, etc), clothes and clothing accessories like ties, belts, or socks, and miscellaneous accessories like key rings, covers for suits, sachets, or umbrellas. It’s worth adding that the company doesn’t produce any of its products themselves but designs, markets, and sells them while the production is outsourced to outside companies. It also sells most of its products in collection ranges like other fashion companies. Some of these ranges are available on an annual and constant basis whilst others are seasonal (e.g. Winter/Autumn and Spring/Summer collections).

Almost half of the company’s revenue is composed of suitcases alone and almost 3 quarters are made out of suitcases and bags (look pie chart below). It’s safe to say that the other product categories are auxiliary. However, they play an important role in improving Wittchen’s brand awareness among consumers. Wittchen is trying to position itself as one of the main luxury players in the market, which is evident in the product’s design as some of them could easily pass as “Gucci ripoffs”.

Nevertheless, Wittchen’s products are much cheaper and its strategy is volume and price based. Investing in clothing and fashion ranges improves the overall brand differentiation and makes the suitcases more attractive as well. As such, despite being auxiliary, other products play a clear part in the strategy.

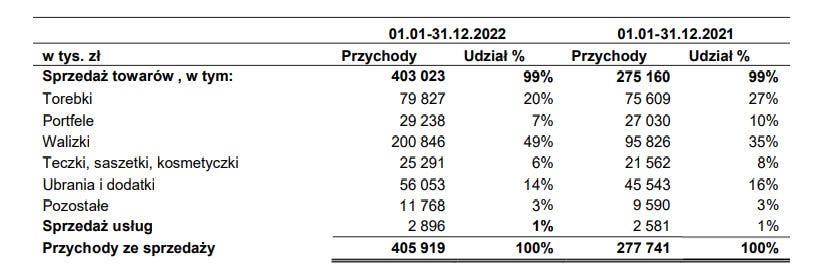

Wittchen typically grows its sales in the mid-double digits during its typical steady years and then has larger surges of 20%+ in some random years (e.g. 2014 & 2017), which is primarily due to its cyclical dependence on the travel demand. If ~50% of your revenue comes from suitcases, you are leveraged on travel demand (high demand equals supernormal profits and low demand...well). Covid hit the company quite badly and the sales have been rebounding since, which has resulted in supernormal and unsustainable rates (32% in 2021 and 46% in 2022). This is mostly due to the suitcase category more than doubling in sales in 2022 as compared to 2021 whilst other categories growing in a more typical and steady fashion.

(2022 Annual Report)

This is the revenue split in 2022 and 2021 presented in the company’s 10k. Suitcases are the third category and the third one from the top (after bags and wallets; then the 5th are clothes and accessories). The year-on-year growth was ~110% and the category went from 35% to 49% share of the total revenue. All of this will be important when we start looking at the company’s track record and valuation.

What remains due is a brief overview of the company’s products. As hinted earlier, Wittchen’s products are not the highest “premium” quality available in the market. They are some of the cheapest ones one can stumble across when strolling through any large shopping mall in Poland. At the same time, they try to offer decent quality at very low prices. The company is predominantly known as a suitcase business and even its brick-and-mortar stores emphasise suitcases with their layouts and other products are shelved in smaller quantities and on the sides.

(Wittchen store in a shopping mall)

Despite below-average prices for all of their products, the range is marketed as quality goods and management has chosen a type of style more associated with higher-end fashion products. This is because Wittchen’s management is trying to transform its image from a suitcase company to a leather fashion brand that transcends suitcases and sells things from wallets and belts to jackets and purses. This is more of a necessity than a ground-breaking innovation as the suitcase market is very cyclical and so have been the company’s sales. By spreading the product channels away from the suitcase, that cyclicality should be slightly mitigated.

Growth Strategy

Keep reading with a 7-day free trial

Subscribe to Bebop Value to keep reading this post and get 7 days of free access to the full post archives.