TOYA S.A. (TOA.WA)

Insider-owned small cap low-cost importer of electric and hand tools buying back shares, selling for a p/e of 8.3x , EV/EBIT of 7x and with a good (conservative) DCF upside.

Key Facts

Description: Toya S.A. is one of the largest brands of hand and power tools for both professional use, such as construction companies, and DIY enthusiasts in Eastern Europe. It has a diversified portfolio with various adjacent products (garden, kitchen, bathroom equipment) and a global supply chain with wholly owned subsidiaries in Romania and China. The latter allows it to export its products cheaply outside of Eastern Europe to Africa, South America and Asia. Its direct online sales channel, with higher margins than traditional ones, is a hidden growth catalyst. The management also started buying back shares. The company was founded in 1990 and is 50.6% insider-owned.

Track record: The company is known for a long-term and steady growth with the 10-year revenue CAGR sitting at 12.6% (5-year 10.9% impacted by the post Covid slowdown as people bought fewer tools, which have a 3 to 5 year lifespan) and the last year’s growth at 12.1% resurrected by the fairly new higher-margin direct online segment. The returns on capital have historically averaged around the upper teens and lower 20s. Moreover, the 10-year CAGR for the EPS and BVPS stands at 12.3% and 13.6% respectively.

Market cap: Its market cap as of the 26th of June 2025 is PLN 636 million ($176 million). It has grown at a CAGR of ~20% over the last 5 years.

Valuation: TOA.WA trades at a TTM P/E of 8.29x (5-year average of 7.4x, although I expect a slight expansion due to the latter-mentioned catalyst) and an EV/EBIT of 7x (5-year average of 6.28x).

Business Overview

Background

Toya manufactures, imports and distributes hand and power tools for both professionals and home use, household and garden equipment, and catering equipment. Most of the products are imported from China. Toya focuses its international (non-Polish) sales in central and eastern European countries like Romania, Ukraine, Baltic Countries, Hungary, Belarus, Moldova, Czechia, Bulgaria and Germany. The company has 3 fully owned subsidiaries: Toya Romania, Yato Tools (Shanghai) and Yato Tools (Jiaxing), which are all involved in its distribution and import process.

Yato Tools (Jiaxing) is based in Baibu Town, Zhejiang, China, which is located right between the two biggest commercial harbours in the world: Shanghai and Ningbo. It’s close to all of the company’s major suppliers and serves as Toya’s main logistics hub. All the tools sold in Europe through Poland and Romania are shipped from there. Toya is looking to expand more into South America and Africa through its Chinese subsidiaries, and the management invested $12.5 million into Yato Tools (Jiaxing) over the last few years in annual trenches.)

(Yato Tools Jiaxing’s HQ)

It’s worth adding that the Chinese subsidiaries don’t produce anything themselves and source production from local suppliers. The subsidiaries then ship them to Poland, Romania and around the world. The process approximates private label production as Toya designs and manages the Yato brand, which is then manufactured by third parties in China, closely supervised by the wholly owned Chinese subsidiaries, who then manage logistics with Toya in Europe.

Product portfolio

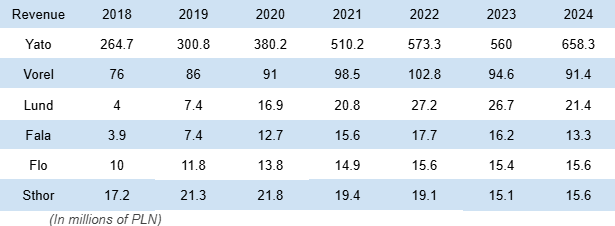

Out of 13,000 products in Toya’s portfolio, 8,300 are under the Yato brand, which gives Yato a 63.8% share in the company’s product portfolio (and an 80% share in the revenue). Toya has multiple private labels: Yato (electric & power tools), Vorel (workshop & construction hand tools), Lund, Sthor, Fala (bathroom equipment) and Flo (garden tools). Private label breakdown by revenue and gross profit:

As you can see, the portfolio is dominated by Yato, which is also driving Toya’s growth. The main marketing strategy is focused on increasing Yato’s share of total revenue, which has grown from 69.5% in 2018 to 80.2% in 2024. Streamlining the product focus on the best-selling brand is what I like to see (instead of the deworsification as Peter Lynch would put it). It also comes with an additional benefit of a faster acquisition of the consumer’s share of mind.

Yato was established by Toya in 2012, and as you might have noticed, it’s the reverse of Toya’s two syllables (to <-> ya). Yato tools are the jack of all trades and include products like socket wrenches, torque and impact wrenches, screwdrivers, pliers, combination wrenches, hammers, drill bits, cutting discs, lighting and health and safety products, etc. Interestingly enough, Toya has a customer overlap with Auto Partner as it also sells automotive workshop equipment, such as cabinets and tool kits, pneumatics and specialised tools for car repair. Yato accounts for 80% of all revenue as of FY 2024.

(Yato Drill Driver)

If Yato is the universal jack-of-all-trades range, then the other brands are specialised in their respective niches. Vorel is similar to Yato, but focused on electric hand tools (11% of revenue), Lund is the kitchen equipment like irons, hoovers, mops, blenders and mixers (4%), Sthor is DIY tools for dads in a garage (2%), Fala is bathroom equipment like shower handles (2%) and Flow is garden equipment like saws, gloves or rakes (2%).

(Fala Soap Dispenser)

Think of Yato as the core brand while all the others as adjacent supporting ones. For example, Yato would sell a lawn mower while Flo would provide composters, plant stringing and lawn edging equipment.

Sales channels (hidden catalyst)

Keep reading with a 7-day free trial

Subscribe to Bebop Value to keep reading this post and get 7 days of free access to the full post archives.